.png)

Why Choose Mutual Funds? – The Smart Investor’s Choice

In our earlier discussion, we covered what a mutual fund is and how it works. Now, let’s take the next step — understanding why mutual funds deserve a spot in your financial plan.

Mutual funds have become one of the most preferred investment options in India, not just for beginners but also for seasoned investors. According to AMFI (Association of Mutual Funds in India), the mutual fund industry’s Assets Under Management (AUM) crossed ₹58 lakh crore in 2024, showing that more Indians are trusting this route to build wealth.

Think of it like going to a grand buffet. Instead of cooking an entire meal yourself (buying one single stock), you contribute along with many others to a professional chef (the fund manager). This chef uses everyone’s contributions to prepare a huge variety of dishes — in investment terms, these are different stocks, bonds, and other assets.

When you invest, you get a plate with a portion of everything — giving you instant variety, balance, and safety in just one step.

For example: If you invest ₹1,000 in a mutual fund, your money — combined with thousands of other investors’ — is invested in companies like Reliance, TCS, HDFC Bank, Infosys, and many more. Your ₹1,000 now owns small pieces of multiple companies, reducing risk compared to owning shares of just one company.

1. Diversification – The Safety Net for Your Money

The golden rule of investing: Don’t put all your eggs in one basket.

Mutual funds make diversification effortless. Instead of you trying to pick a single winning company, you get a ready-made basket containing small portions of many companies. If one company doesn’t do well, others help balance it out

Example:

If you put ₹10,000 in one stock and it falls 30%, your loss is ₹3,000.

But if you invest ₹10,000 across different stocks via a mutual fund, one stock’s fall will hardly affect your overall portfolio.

Tip: Don’t stop at one mutual fund. Build a portfolio with different types of funds — like equity, debt, and hybrid — so you spread your risk across companies, sectors, and asset classes.

2. Transparency – You Always Know Where Your Money Is

One of the most reassuring parts of mutual funds is their complete transparency.

Before you invest, you receive:

- Scheme Information Document (SID) explaining objectives, risks, and costs

- Key Information Memorandum (KIM) summarising key facts about the fund

Once invested, you can:

- Check your daily NAV online

- View monthly factsheets showing every stock or bond the fund holds

- Get performance reports and audited statements regularly

In India, SEBI (Securities and Exchange Board of India) strictly regulates mutual funds to ensure fairness and protect investors. SEBI mandates that all fees, charges, and investment holdings be disclosed openly — so you’re never left in the dark about where your money is going.

3. Professional Fund Management – Let Experts Do the Heavy Lifting

Managing investments is not easy — it requires research, analysis, and constant monitoring.

When you invest in a mutual fund, your money is managed by a qualified fund manager and a team of analysts. They:

- Study companies and markets daily

- Monitor global and domestic trends

- Adjust the portfolio to protect and grow your wealth

Many top fund managers in India have over 20 years of experience and manage funds worth thousands of crores. They have access to advanced research tools, corporate insights, and economic data that the average investor cannot easily obtain.

Benefit: You don’t need to spend hours analysing financial reports — your investments are in professional hands.

4. Goal-Based Flexibility – One Tool for All Your Dreams

Everyone’s financial goals are unique:

- Short-term: Saving for a vacation or buying a car

- Medium-term: Funding a child’s education or starting a business

- Long-term: Retirement planning or building a legacy

Mutual funds offer a variety of categories for each goal:

- Debt funds for low-risk, short-term needs

- Hybrid funds for a balanced approach

- Equity funds for high growth over the long term

This flexibility means you can customise your portfolio like a menu — selecting the right mix for your needs. For example, a 30-year-old saving for retirement might have 80% in equity funds and 20% in debt funds, while a retiree might flip that ratio to focus on stability and income.

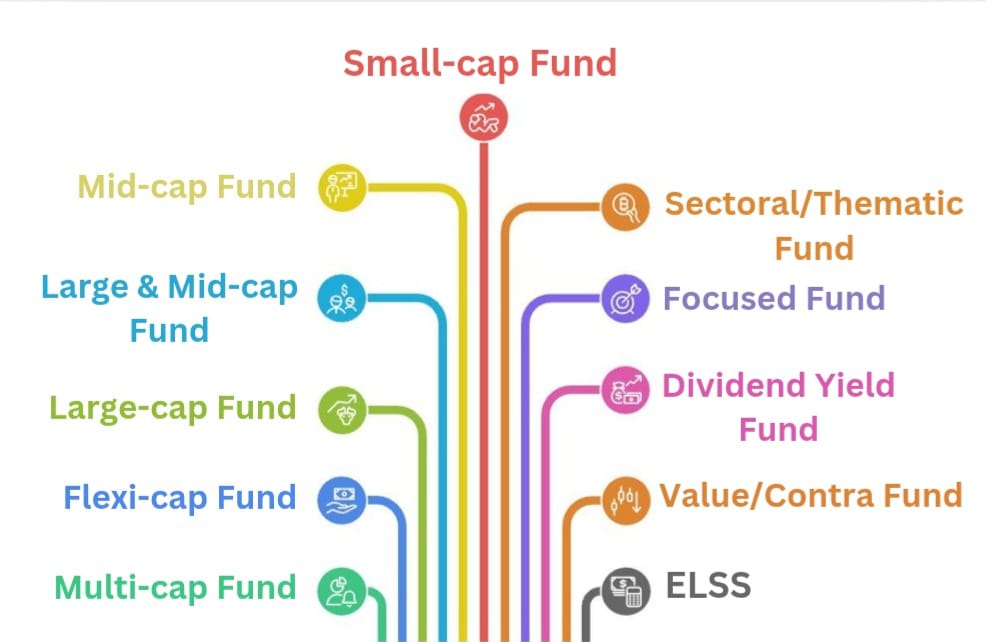

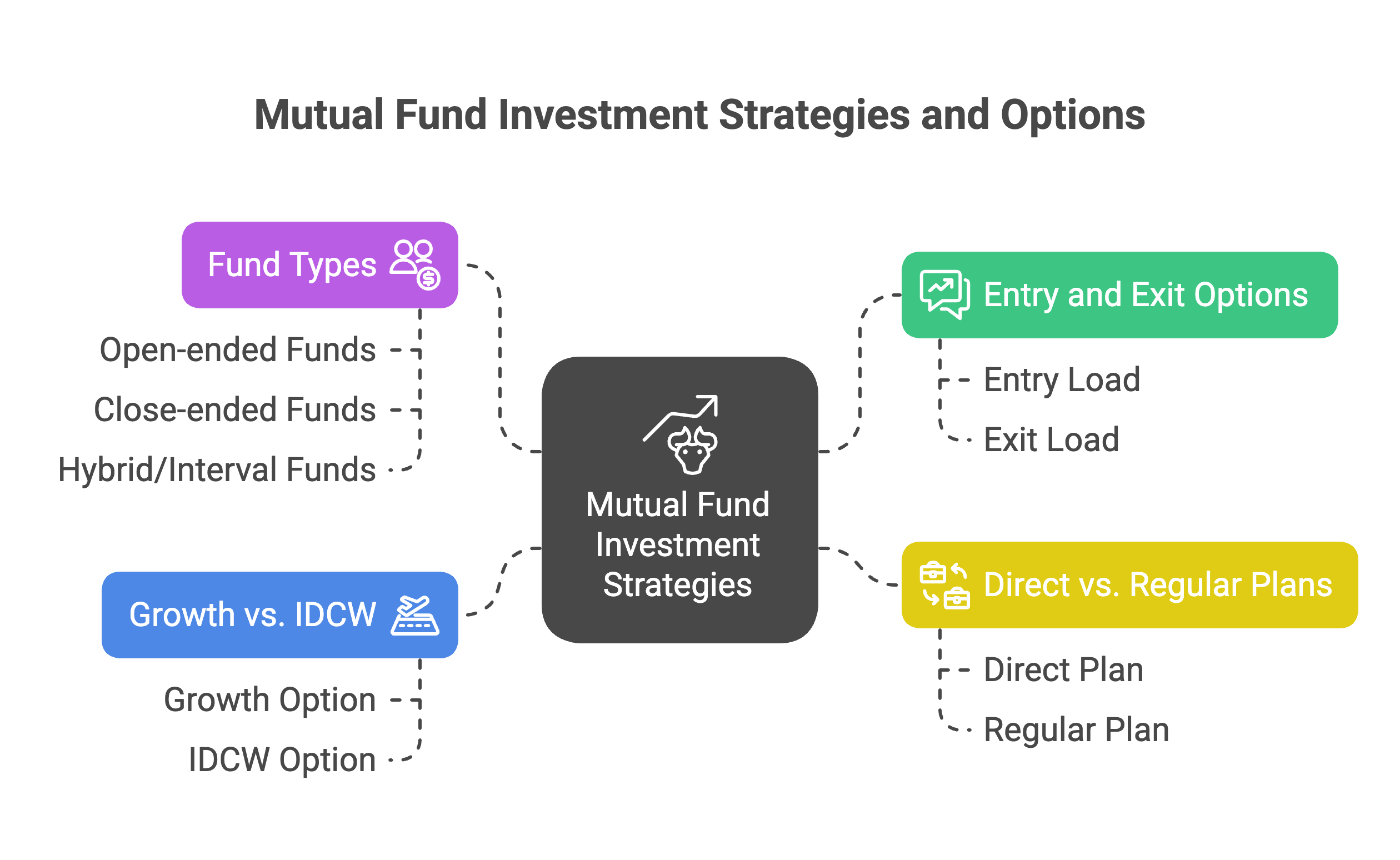

5. Options for Every Investor Type

Whether you’re cautious or adventurous, there’s a mutual fund for you.

Types of Funds:

- Equity Funds: High risk, high return potential, best for long-term growth

- Debt Funds: Lower risk, steady returns, ideal for short-term or emergency funds

- Hybrid Funds: A mix of equity and debt for balanced performance

- Index Funds & ETFs: Passive, low-cost options that track market indices

You can even choose thematic or sectoral funds if you have a strong view about a specific industry (like technology or healthcare), or international funds to gain exposure to global markets.

6. Pathway to Financial Freedom

Financial freedom isn’t just about having a lot of money — it’s about having choices.

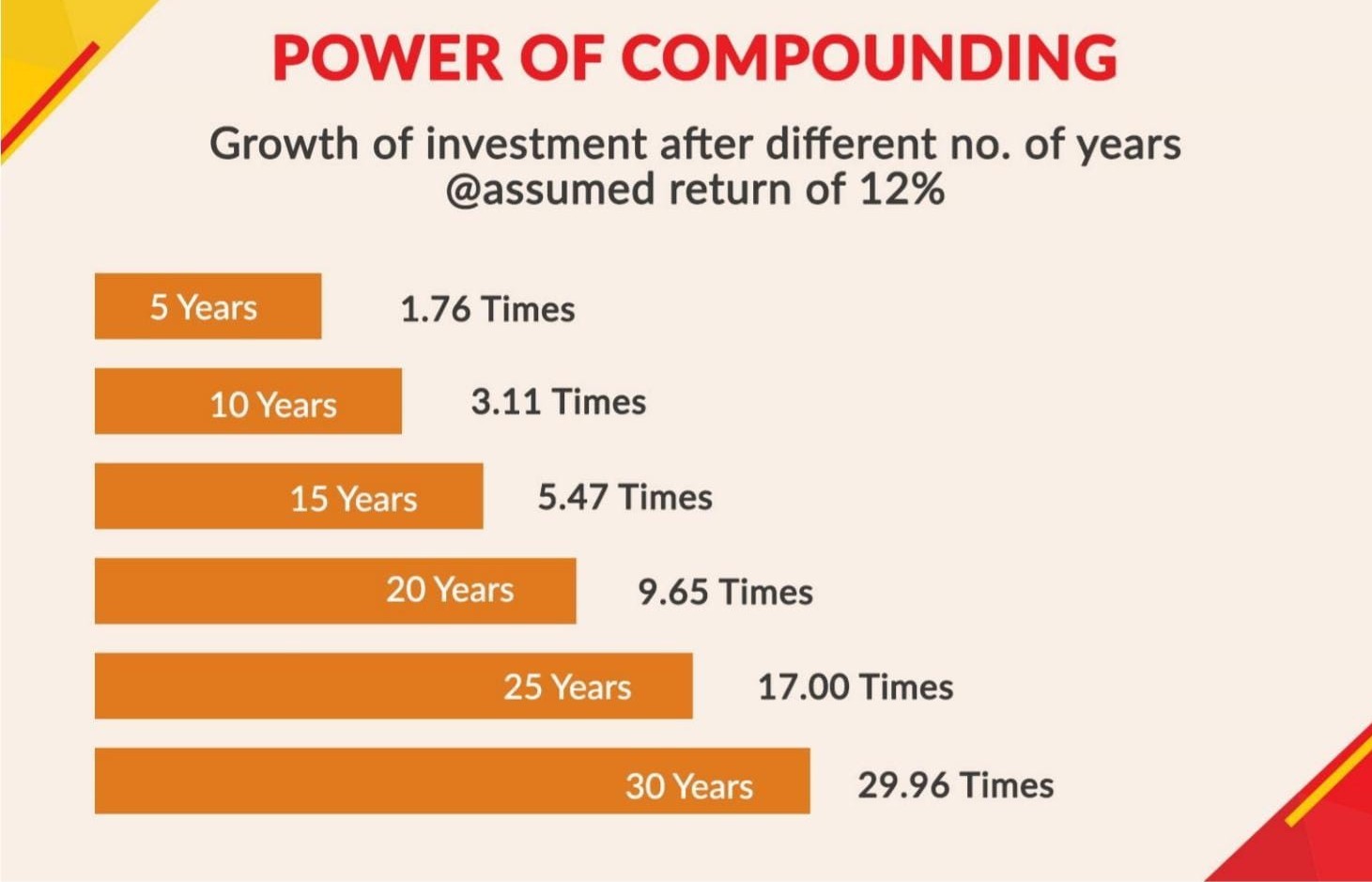

Through disciplined investing, especially via SIPs (Systematic Investment Plans), mutual funds help you:

- Harness the power of compounding — where returns generate more returns

- Outpace inflation over time

- Build a corpus big enough to support your lifestyle without relying on active income

? A simple ₹5,000/month SIP in an equity mutual fund with 12% annual returns can grow to over ₹1.77 crore in 30 years. That’s the power of consistency and time.

7. Liquidity – Access Your Money When You Need It

Most mutual funds, especially open-ended funds, allow you to redeem your investment at any time on business days. The amount is usually credited to your bank account within 1–3 working days.

This makes them more flexible than fixed deposits (FDs) or real estate, where early withdrawal can mean penalties or delays. However, some funds (like ELSS – Equity Linked Savings Schemes) have a lock-in period, which also helps in building discipline.

8. Cost-Effective Investing

Mutual funds pool money from many investors, which means costs are spread out. Fund houses can negotiate lower transaction fees, and investors benefit from economies of scale.

In India, many direct mutual fund plans have expense ratios as low as 0.2%–1%, making them far more cost-efficient than traditional investment products.

Conclusion – Why Mutual Funds Deserve a Place in Your Portfolio

Mutual funds combine diversification, transparency, professional management, flexibility, and cost efficiency — making them one of the most powerful wealth-building tools available to investors today.

Whether you’re starting with ₹500/month or ₹50,000/month, the key is to start early, stay consistent, and let time work its magic.

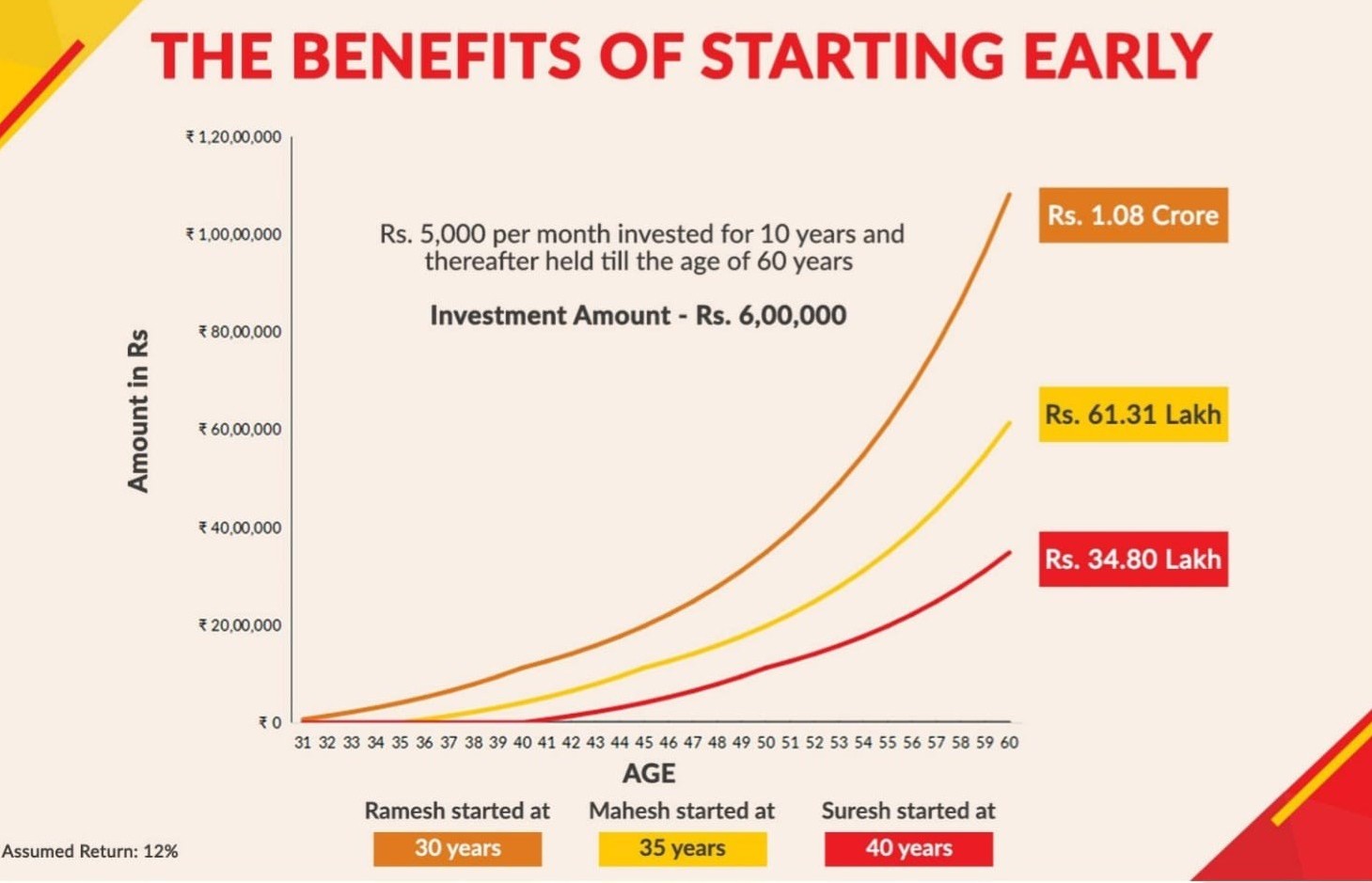

An Example for a Long-Term Goal: Planning for Retirement

Let's imagine two friends, Arjun and Rohit, both 35 years old. They both have the same dream: to build a large enough corpus to retire comfortably at the age of 60. They each decide they can set aside ₹5,000 per month.

1) Arjun's Path: The Long- Term Investor:

Arjun understands that to beat inflation and create real wealth, he needs his money to grow significantly. He chooses to invest her ₹5,000 every month into an equity mutual fund through a SIP. He knows there will be ups and downs, but He stays invested for the long term. Let's assume her investment grows at an average of 12% per year.

Arjun is cautious. He decides to put his ₹5,000 every month into a combination of "safe" options like Recurring Deposits (RDs) and other fixed-income schemes. Let's assume he gets an average return of 6% per year over the long run.

- Over 35 years (from age 25 to 60), he diligently saves.

- His total investment is ₹15 Lakhs (₹5,000 x 12 months x 35 years).

- At a 12% return, his corpus grows to approximately ₹95 Lakhs.

2) Rohit’s Path: The "Safe" Saver

ROHIT is cautious. He decides to put his ₹5,000 every month into a combination of "safe" options like Recurring Deposits (RDs) and other fixed-income schemes. Let's assume he gets an average return of 6% per year over the long run.

- Over the same 35 years, her total investment is also just ₹15 Lakhs.

- However, thanks to the power of compounding, her investment grows exponentially.

- At a 12% return, his retirement corpus grows to an ₹35 Lakhs.

The Lesson:

Both started with the same small amount and had the same goal. But by choosing to invest, Arjun allowed his money to work for his. For long-term goals, simply saving is a losing battle against inflation. Investing is the engine that uses time and compounding to turn small, regular savings into life-changing wealth.

Note: Mutual funds are subject to market risks. Read all scheme documents carefully. Past performance is not indicative of future returns.

.png)

.png)

.png)

.png)